For those of you who heard, there was recently a price increase in Netflix's services. It began offering its streaming and DVD services separately. Those who continued to use both services saw an effective price increase of 60%.

Lo and behold, Netflix came out today and announced that its profits would be only 72 cents to $1.07 a share, compared to analysts' projections of $1.11 a share. Sales are also projected to be only $828.5 million instead of the analysts' expectation of $842.9 million.

So what went wrong? For one thing, Netflix forgot to take into effect one of the most fundamental pillars of economics: the law of demand. It evidently forgot that as prices increase, quantity demanded decreases. Considering the fact that a goods like online streaming and DVD rental, both markets with numerous competitors, can be expected to be relatively elastic in demand, it is somewhat surprising that Netflix's management managed to overlook this critical fact. The result? A vote of no confidence in Netflix's management.

Common Knowledge

Friday, April 15, 2011

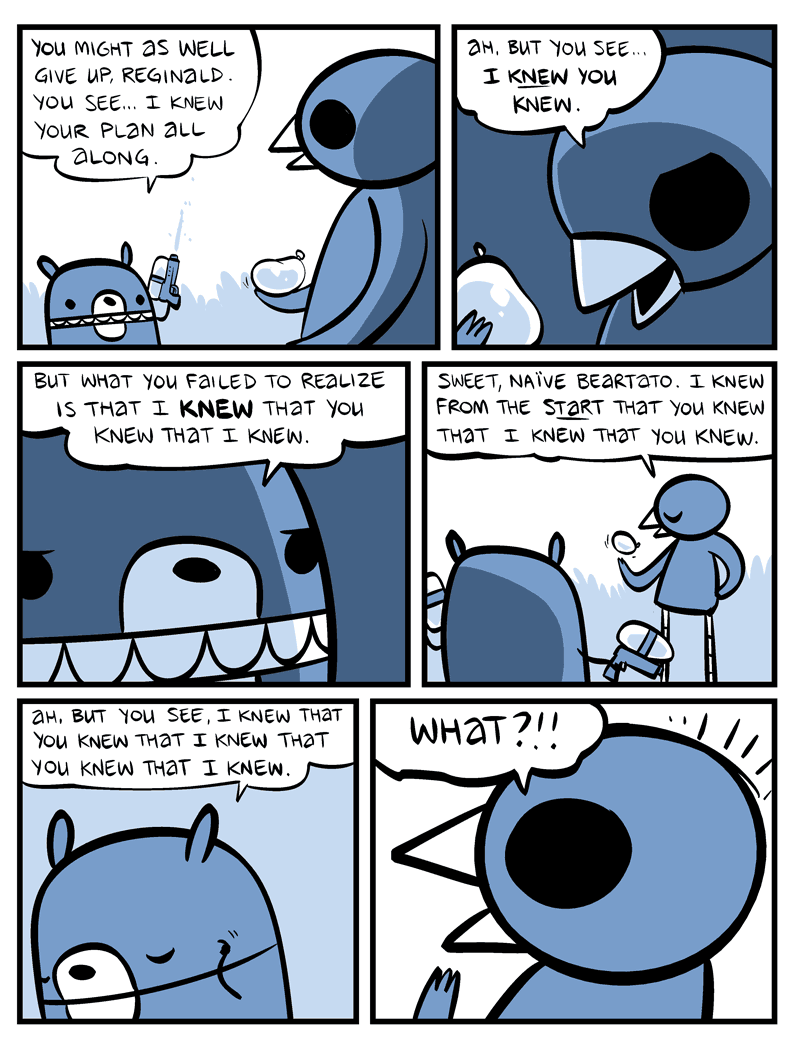

What is common knowledge? Economists tend to talk about "perfect information." It implies that certain information is common knowledge among participants within a certain market transaction. Game theory draws upon the concept of common knowledge in analyzing games with asymmetric information. For a functional, albeit mathematical definition of common knowledge, we turn to logic theory. The basic principle is perhaps confusing at first, but the concept is extremely important in both economics and logic theory.

Below is a comic (courtesy of Nedroid) that demonstrates the concept, though for something to be truly common logic, the process must continue ad infinitum.

Below is a comic (courtesy of Nedroid) that demonstrates the concept, though for something to be truly common logic, the process must continue ad infinitum.

A Theory of Interstellar Trade

Thursday, February 10, 2011

This paper is pretty old, but I just took the time to read it. Very interesting, and courtesy of Krugman.

The Wallet Paradox

Wednesday, February 9, 2011

Another classic game theory puzzle, this time with a different twist. Here's the basic setup:

Think about this game for a while. The solution is here.

Bill Gates meets Warren Buffett at a dinner party and the host tells them to play a game. Each person will place his wallet on the table. The person with less money in his wallet wins all the money.

Is anyone favored to win this game?

...Afterwards, it turns out both Bill Gates and Warren Buffett loved the game.

They add a twist as follows. They will play the game every day for a month. To manage the stakes, they agree to carry an average (mean) of $100. Is this game fair? What is the best possible strategy, given you know what your opponent is doing?

Is the Economy Growing Too Fast?

Tuesday, February 8, 2011

For the past year or so, the Fed has been forecasting a timid recovery with little upward price pressures. Are things going better than expected? But more importantly, are the latest growth numbers going to signal to the fed that this period of extraordinary expansionary monetary policy is over? A good analysis is here.

Interactive Global Inflation Chart

Wednesday, February 2, 2011

The Wall Street Journal provides this graphic that shows inflation rates in nations around the world during the recession. You can really gain a good perspective about the risk of deflation in many countries through this period. This perhaps is more evidence for the strength and duration of the Fed's response to the recession.

A Game Theory Puzzle

Tuesday, February 1, 2011

A game theory puzzle from an interesting new blog I found:

The solution is a very interesting application of game theory. The solution can be found here.

"On a game show, two people are assigned whole, positive numbers. Secretly each is told his number and that the two numbers are consecutive. The point of the game is to guess the other number.

Here are the rules of the game:

–The two sit in a room which has a clock that strikes every minute on the minute

–The players cannot communicate in any way

–The two wait in the room until someone knows the other person’s number. At that point, the person waits until the next strike of the clock and can announce the numbers

–The game continues indefinitely until someone makes a guess

–The contestants win $1 million if correct, and nothing if they are wrong

Can they win this game? If so, how?"

The solution is a very interesting application of game theory. The solution can be found here.

Mankiw On Education

Monday, January 24, 2011

I think that these reflections say a lot not only for graduate education, but for a lot of educational choices in life. Link here.

Taylor on Rule Based Monetary Policy

Saturday, January 15, 2011

Here is a speech by John B. Taylor regarding the relative merits of rule based monetary policy. The link is here.

If you are interested in monetary theory and know anything about the Taylor Rule, you may find this speech very interesting. Taylor has long been a proponent of rule based monetary policy. The topic is one that deserves much debate, so don't take everything Taylor says as truth.

If you are interested in monetary theory and know anything about the Taylor Rule, you may find this speech very interesting. Taylor has long been a proponent of rule based monetary policy. The topic is one that deserves much debate, so don't take everything Taylor says as truth.

Yellen on QE2

Thursday, January 13, 2011

In a speech by Janet Yellen at the Brimmer Policy Forum, Yellen gave the fed's rationale for QE2. Some interesting excerpts are below:

"As shown in figure 1, the unemployment rate rose from around 5 percent in the spring of 2008 to about 10 percent by the autumn of 2009 and has stayed well above 9 percent since then. Most observers, including myself, judge this level of unemployment to be much higher than levels consistent with full employment and stable inflation... In addition, a historically large fraction of the unemployed have been out of a job for a very long time. For example, roughly 4 percentage points of today's unemployment rate reflects individuals who have been unemployed for half a year or more. Those who experience an extended period of unemployment face a risk of losing their ability to participate successfully in the workforce, lending additional urgency to the task of reviving the demand for labor."The high unemployment rate and low levels of capacity utilization have been the Fed's go to reason for the necessity of QE2. What surprises me is that Yellen did not cite weakness in housing markets as a reason for QE2. However, Yellen does continue on to a discussion of long term assets, which directly affect housing markets in the form of long term interest rates.

"As shown in figure 4, longer-term Treasury yields have risen substantially over the past couple of months since the FOMC initiated this round of asset purchases. I believe that this increase in Treasury yields likely reflects a number of significant factors, including incoming information suggesting a somewhat stronger economic outlook and the fiscal package that was announced by President Obama in early December and approved by the Congress about two weeks later; that package will not only support economic growth next year but will also increase the amount of federal debt issuance. Also, investors appear to have scaled back their expectations about the extent to which the FOMC will engage in further purchases beyond those already announced; however, the effect of that reassessment on market rates tends to bolster the view that the Federal Reserve's securities purchases do indeed affect yields in the direction indicated by analytical and empirical studies."One point (that was also made by Duke) is the fact that QE2 is meant more as a way of maintaining the Fed's expansionary policy rather than furthering it. However, this speech actual cites evidence for this claim. This point is interesting, and perhaps under stated.

"In contrast, I disagree with the notion that the large quantity of reserves resulting from our asset purchases poses some special barrier to removing policy stimulus when the right time comes. The FOMC will be able to increase short-term rates by raising the interest rate that we pay on excess reserves--currently 1/4 percent. That ability will allow us to manage short-term interest rates effectively and thus to tighten policy when needed, even if bank reserves remain high."Once again, another major player in the federal reserve system has openly stated the role of interest on reserves in keeping inflation in check. The more I read and the more I think about it, the more I am convinced that the interest of reserves policy tool will become the new tool of choice for the Fed in the period that it will take for the economy to recover. The implications for this are profound. It essentially says that the Fed will be able to keep toxic assets on its balance sheet for an extended period without lowering the effective interest rate in the economy.

Duke on QE2

Monday, January 10, 2011

In the span of a few days, many major players from inside the Fed have offered their insights on the current state of the economy and the mechanisms through which the fed plans to pull out of this recession. The following are interesting excerpts from Elizabeth Duke's speech regarding current economic conditions and monetary policy:

"My outlook for the housing market and for commercial real estate is more cautious. A sustained recovery in income and jobs will be an important prerequisite for a recovery in the housing industry. But until the overhang of vacant homes is reduced significantly and home values begin to firm, new residential construction is likely to remain at low levels. Similarly, time will be required to absorb the currently large amount of vacant office and commercial space before construction in that sector begins to turn up noticeably."First, it is very clear that the Fed is very worried about the continued high rate of unemployment and sustained weakness in the housing market.

"One notable exception to my forecast for gradual improvement in financial markets is my expectation that residential mortgage markets could take a number of years to repair as policymakers and market participants grapple with the role of government in housing finance, adapt to changing regulation, and look for ways to better manage and price the risks associated with mortgage lending and servicing. Whatever the structure of housing finance is to become, the large overhang of problem loans and weak housing markets will necessitate a gradual transition."I find this point to be very interesting. If residential mortgage markets do not recover significantly in the near future, it could mean that the Fed will continue to hold its Mortgage Backed Assets for an extended period of time until those respective financial markets stabilize.

"...between December 2008 and March 2010, the FOMC elected to purchase large amounts of longer-term Treasury, agency, and agency mortgage-backed securities (MBS). Those purchases put downward pressure on longer-term interest rates generally and helped normalize the spread between mortgage rates and long-term Treasury rates, which had widened during the financial crisis. Reducing longer-term rates influences the economy in much the same way as lowering the expected path of short-term rates. For instance, the decline in longer-term rates lowers the cost and increases the availability of capital and credit, which in turn encourages business expansion. In the most recent episode, another important result of lower rates has been a reduction in debt service burdens from existing debt. Households in particular have significantly reduced mortgage payments through refinancing. And numerous small business owners have told me that they could not have survived the downturn without low rates.

Economic activity picked up in early 2010, but by the time the FOMC met in August, the rate of growth seemed to be slowing and inflation continued to drift lower. In addition, lower mortgage rates were resulting in faster prepayment of mortgages underlying the agency MBS held by the Federal Reserve. To avoid the modest monetary tightening that would result from the Fed's gradually shrinking portfolio of agency MBS, the FOMC voted to reinvest all principal payments from agency debt and agency MBS in longer-term Treasury securities. The Committee also began a discussion about the strength of the recovery, the amount of slack in the economy, the likely path of inflation, and the appropriate action to provide additional monetary accommodation should such action be deemed necessary. In November, the FOMC judged that additional monetary policy stimulus was needed to support the economic recovery and help ensure that inflation, over time, returned to desired levels. To implement that stimulus, the Committee decided to expand its holdings of securities by purchasing an additional $600 billion in longer-term Treasury securities by the end of the second quarter of 2011.

After considering the costs and benefits of the action and recognizing that taking no action would have its own risks, I believe that the expansion of securities holdings was worth implementing to support the economy and make the recovery more durable. I don't want to overpromise. This action is not a panacea. While it is still premature to judge the overall efficacy of the program, I believe that by exerting downward pressure on longer-term interest rates, it has provided and will continue to provide support for a vulnerable recovery. At the same time, I believe the risks associated with this action are manageable, that we have the safeguards in place to monitor evolving conditions, and, most importantly, that we have the conviction to act when necessary.

Based on our own research and that of others, evidence is accumulating that purchases of longer-term assets have been successful in exerting downward pressure on longer-term rates.1Consistent with research on the effects of asset purchases, between August, when Chairman Bernanke in a speech first publicly suggested the Federal Reserve might take additional action, and November, when the action was taken, longer-term Treasury rates fell as market participants priced in additional Fed purchases.2 However, since the announcement of the decision to purchase longer-term Treasury securities, longer-term rates have actually increased. It might seem that the recent increase in rates contradicts the view that Fed asset purchases put downward pressure on rates. However, the logic behind this view works in both directions. If the market expects the Fed to respond to weak economic conditions by buying more assets, investors bid up the assets and rates fall. Conversely, if the market expects the economy to strengthen, investors ratchet back expectations for Fed purchases and reduce their bid for the assets, and rates rise. I believe that the current rise in rates is due to exactly this latter circumstance--a strengthening in market participants' outlook for the economy and a corresponding decrease in the market's expectation for future accommodation."This section explains the Fed's rationale for quantitative easing, which have been pretty well established before. However, one point draws my attention. Duke claims that partly due to recovery, home owners have been paying back mortgages at an increasing rate, decreasing modestly the profile of the Fed's balance sheet in mortgage backed securities. This would have, at least on some level, provided a contractionary effect in financial markets. This is a point that I have not heard anyone make yet.

"The monetary policy objective of asset purchases is to foster downward pressure on interest rates. But assets are "paid for" by crediting the reserve balances of banks, generating higher levels of reserve balances in the banking system. Reserves are relevant to the growth of the money supply because banks are required to hold a percentage of some types of deposits as reserves with the Federal Reserve. Thus, the total amount of reserves in the banking system acts to cap maximum reservable deposits. It is important to note that it is deposits, not reserve balances, that are included in the monetary aggregates used to measure the money supply. For example, M1 is made up of currency, traveler's checks, demand deposits, and other checkable deposits, while M2 is made up of M1 plus savings, small time deposits, and retail money market mutual funds.

Moreover, the linkage between the level of reserve balances and the monetary aggregates in the current environment is quite weak. You were probably taught, as I was, that the broad monetary aggregates increase when reserve balances increase because the larger volume of reserves supports increased lending, which in turn leads to a larger volume of reservable deposits. While that argument might hold in normal circumstances, in the current environment excess reserves are many multiples of required reserves, and adding reserves is unlikely to spark a further increase in the volume of deposits. As a result, the textbook linkage between reserve balances, bank loans, and transaction deposits just is not operative at present. Fundamentally, the levels of M1 and M2 are determined by the strength of the economy and the preferences of businesses and consumers for money, which depend on the yields on monetary instruments and competing assets.

Recent experience has again illustrated the difficulty in identifying a reliable relationship between reserve balances and the monetary aggregates. Even though Federal Reserve actions to fight the financial crisis and support the economic recovery added roughly $1 trillion to a base of about $43 billion in aggregate bank reserves, M1 and M2 rose at relatively moderate rates over the same period.

Going one step further, I should note that the linkage between the monetary aggregates and either real economic activity or inflation has been very weak over recent decades. The lack of a reliable relationship between the monetary aggregates and the economy led the Federal Reserve to abandon M1 as a key policy instrument in the early 1980s and then to reduce the role of M2 as a policy instrument in the late 1980s and early 1990s. Indeed, in a 2006 speech about the historic use of monetary aggregates in setting Federal Reserve policy, Chairman Bernanke pointed out that, "in practice, the difficulty has been that, in the United States, deregulation, financial innovation, and other factors have led to recurrent instability in the relationships between various monetary aggregates and other nominal variables."3 Still, my colleagues and I will be monitoring a wide range of financial and economic developments very closely--including the growth of the money supply, inflation, and many other financial and nonfinancial variables--and, based on a full assessment of those developments, the FOMC will withdraw monetary accommodation at the appropriate time. My view is that the elevated reserve balances would be inflationary only if they prevented the FOMC from effectively removing monetary accommodation by raising interest rates when the time comes to remove such accommodation, and I am convinced that that will not be the case.

The FOMC has a number of tools at its disposal for raising interest rates. When appropriate, the Federal Reserve can put upward pressure on interest rates by raising the rate it pays on reserve balances. Moreover, we have developed new tools that will allow us to drain reserves if necessary. In particular, we can drain large volumes of reserves by replacing them with repurchase agreements and term deposits. Finally, we can always sell the securities we purchased. Such sales would not only drain reserves but would also put direct upward pressure on longer-term rates."Once again, we have a very high profile member of the Fed vouching for the use of interest on reserves a policy tool in preventing inflation from getting out of hand. Over the past year, many agents from the Fed have begun to put an increasingly large amount of emphasis on this tool. The tool was originally conceived to serve as a floor on market interest rates (just as the discount window serves as a ceiling). However, Bernanke in a speech last year claimed that the Fed was looking into an alternative interest rate of some sort. I am beginning to wonder if this new interest on reserves tool will be made into the new standard for interest rates.

Bernanke on QE2

As a part of his testimony before the Senate Budget Committee, Ben Bernanke made the following remark:

Conventional monetary policy works by changing market expectations for the future path of short-term interest rates, which, in turn, influences the current level of longer-term interest rates and other financial conditions. These changes in financial conditions then affect household and business spending. By contrast, securities purchases by the Federal Reserve put downward pressure directly on longer-term interest rates by reducing the stock of longer-term securities held by private investors.3 These actions affect private-sector spending through the same channels as conventional monetary policy. In particular, the Federal Reserve's earlier program of asset purchases appeared to be successful in influencing longer-term interest rates, raising the prices of equities and other assets, and improving credit conditions more broadly, thereby helping stabilize the economy and support the recovery.

In light of this experience, and with the economic outlook still unsatisfactory, late last summer the FOMC began to signal to financial markets that it was considering providing additional monetary policy accommodation by conducting further asset purchases. At its meeting in early November, the FOMC formally announced its intention to purchase an additional $600 billion in Treasury securities by the end of the second quarter of 2011, about one-third of the value of securities purchased in its earlier programs. The FOMC also maintained its policy, adopted at its August meeting, of reinvesting principal received on the Federal Reserve's holdings of securities.

The FOMC stated that it will review its asset purchase program regularly in light of incoming information and will adjust the program as needed to meet its objectives. Importantly, the Committee remains unwaveringly committed to price stability and, in particular, to maintaining inflation at a level consistent with the Federal Reserve's mandate from the Congress.4 In that regard, it bears emphasizing that the Federal Reserve has all the tools it needs to ensure that it will be able to smoothly and effectively exit from this program at the appropriate time. Importantly, the Federal Reserve's ability to pay interest on reserve balances held at the Federal Reserve Banks will allow it to put upward pressure on short-term market interest rates and thus to tighten monetary policy when needed, even if bank reserves remain high. Moreover, the Fed has invested considerable effort in developing methods to drain or immobilize bank reserves as needed to facilitate the smooth withdrawal of policy accommodation when conditions warrant. If necessary, the Committee could also tighten policy by redeeming or selling securities on the open market.Of special interest is Bernanke's interpretation of the new interest on reserves policy tool in the final paragraph. Especially interesting is that in light of all of the Fed's expanded tools throughout the recession, Bernanke chose to highlight this tool in particular as a integral part of controlling inflation throughout the recovery. Also of note is the fact that Bernanke highlights exactly the fact that I made in my previous post: given that lending picks up, the Fed plans to use its interest on reserves policy tool as a means of raising the opportunity cost for lending in order to effectively raise interest rates without forcing itself to introduce toxic assets back into financial markets.

My Thoughts on QE2

Tuesday, January 4, 2011

By now, I think that everyone has heard of the Fed's second round of Quantitative Easing. I saw the news quite a while back, but wanted to wait a bit and read more about the Fed's new move before making a judgment call regarding its policy.

I think one main point that needs to be made right off the bat is that Quantitative Easing is not all that different from traditional open market operations. The difference here is a question of magnitude, not precedence. The much coined phrase of the Fed "printing money" is flawed in that the Fed prints money any time it engages in expansionary open market purchases. The attribute that makes QE2 special is that the Fed is "printing money" to the tune of $600 billion.

It must also be noted that QE2 is not the same as the first round of quantitative easing. A large majority of the first round of quantitative easing consisted of the Fed's purchase of Mortgage Backed Securities (MBS) from the open market (MBS are not Treasury bonds, but private sector assets backed by mortgages). The purpose of such purchases was mainly to decrease the risk premium on interest rates by taking highly risky assets out of financial markets in order to stabilize said financial markets. At the same time, the expansion of the monetary base provided much needed liquidity to banks in the wake of a liquidity crisis. That is, the main purpose of QE1 was to decrease the risk profile of assets in financial markets and provide banks with relief liquidity.

So what exactly is different this time? For starters, the liquidity crisis is nowhere to be found. With a reserve boost of almost $2 trillion from the first round of QE, there is no shortage of liquidity for banks. Also, the Fed is not purchasing MBS from the private sector this time around, opting instead for long term Treasury bonds.

What does this mean? Put simply, QE2 has a completely different purpose than QE1. In the wake of recovery (most would agree that we are in recovery), one of the main factors constraining sustained growth is the housing market. Through purchases of long term treasuries, the Fed is attempting to lower the interest rate for long term assets. This will in turn make it easier for home buyers to finance a new home (and for existing home owners to refinance). In other words, the main purpose of QE2 is to give a much needed boost to the ailing housing sector.

However, I think the main point that most economists are concerned about is the potential for inflation when the monetary base has already been expanded to epic proportions. In that regard, I believe that the Fed has more of a handle on inflation than most economists give it credit for. First of all, it is clear that despite previous expansion of the monetary base, short term inflation expectations continue to remain subdued. But even when lending begins to pick up, I believe the Fed will still be able to keep inflation in check.

The reason for this is the Fed's new tool of interest on reserves. The tool effectively allows the Fed to set a floor on interest rates. As such, should lending pick up, the Fed can simply set the interest on reserves above the Federal Funds Rate to decrease lending. Such action will prevent the somewhat excessive monetary base from translating into a change in the money supply, and by extension, an increase in the inflation rate. This policy will also prevent the reentry of risky assets into financial markets because it does not necessitate the reintroduction of risky assets on the Fed's balance sheet through open market sales, something that could pose highly problematic for an economy in strong rebound.

The verdict? I think the Fed has it under control. I really hope I'm right.

I think one main point that needs to be made right off the bat is that Quantitative Easing is not all that different from traditional open market operations. The difference here is a question of magnitude, not precedence. The much coined phrase of the Fed "printing money" is flawed in that the Fed prints money any time it engages in expansionary open market purchases. The attribute that makes QE2 special is that the Fed is "printing money" to the tune of $600 billion.

It must also be noted that QE2 is not the same as the first round of quantitative easing. A large majority of the first round of quantitative easing consisted of the Fed's purchase of Mortgage Backed Securities (MBS) from the open market (MBS are not Treasury bonds, but private sector assets backed by mortgages). The purpose of such purchases was mainly to decrease the risk premium on interest rates by taking highly risky assets out of financial markets in order to stabilize said financial markets. At the same time, the expansion of the monetary base provided much needed liquidity to banks in the wake of a liquidity crisis. That is, the main purpose of QE1 was to decrease the risk profile of assets in financial markets and provide banks with relief liquidity.

So what exactly is different this time? For starters, the liquidity crisis is nowhere to be found. With a reserve boost of almost $2 trillion from the first round of QE, there is no shortage of liquidity for banks. Also, the Fed is not purchasing MBS from the private sector this time around, opting instead for long term Treasury bonds.

What does this mean? Put simply, QE2 has a completely different purpose than QE1. In the wake of recovery (most would agree that we are in recovery), one of the main factors constraining sustained growth is the housing market. Through purchases of long term treasuries, the Fed is attempting to lower the interest rate for long term assets. This will in turn make it easier for home buyers to finance a new home (and for existing home owners to refinance). In other words, the main purpose of QE2 is to give a much needed boost to the ailing housing sector.

However, I think the main point that most economists are concerned about is the potential for inflation when the monetary base has already been expanded to epic proportions. In that regard, I believe that the Fed has more of a handle on inflation than most economists give it credit for. First of all, it is clear that despite previous expansion of the monetary base, short term inflation expectations continue to remain subdued. But even when lending begins to pick up, I believe the Fed will still be able to keep inflation in check.

The reason for this is the Fed's new tool of interest on reserves. The tool effectively allows the Fed to set a floor on interest rates. As such, should lending pick up, the Fed can simply set the interest on reserves above the Federal Funds Rate to decrease lending. Such action will prevent the somewhat excessive monetary base from translating into a change in the money supply, and by extension, an increase in the inflation rate. This policy will also prevent the reentry of risky assets into financial markets because it does not necessitate the reintroduction of risky assets on the Fed's balance sheet through open market sales, something that could pose highly problematic for an economy in strong rebound.

The verdict? I think the Fed has it under control. I really hope I'm right.

Split or Steal?

Sunday, January 2, 2011

From 2008 to late 2009, there was a game show in Britain called "Golden Balls." At the end of the game, the two contestants are presented with the choices of whether to "Split" or "Steal." The basic concept is explained pretty well by the video below:

A quick glance at the comments show that most viewers were not too pleased with the female player's choice to steal. However, let's take a look at the payoff matrix of this game:

Note that I decided to change the jackpot to 100,000 euros for mathematical simplicity (it's actually 100,150 euros). This situation is slightly different from your typical prisoner's dilemma game, chiefly due to the presence of weak dominance (a case where a the payoff of a strategy is always equal or greater than the payoffs of another strategy as opposed to strict dominance, where the payoff of a strategy is always greater than that of another).

Because the game is symmetrical, I will proceed to analyze the payoffs of only the male player. Note that the payoffs are the exact same for the female player. Given that the female player chooses to split, the best response of the male player is to steal, as a payoff of 100,000 is greater than a payoff of 50,000. If the female player chooses to steal, the male player is indifferent between choosing split or steal. In this game, the male player's strategy of "steal" weakly dominates his strategy of "split."

However, note that this simple analysis is not complete. Because of the existence of weak dominance, two other Nash Equilibria exist: the outcome where the male splits and the female steals, and the case where the male steals and the female splits. If the reason for this is unclear to you, think about the definition for a Nash Equilibrium. The necessary condition for a Nash Equilibrium states that no player can have a profitable deviation. In the outcome where the female splits and the male steals, neither player can increase their payoff by changing his strategy, taking the other player's strategy as given.

The interesting thing about this is that because both "split" AND "steal" are best responses to a particular strategy, the possibility of a mixed strategy Nash Equilibrium arises. A mixed strategy is a scenario where more than one strategy is played at an equilibrium probability (think about a game of rock paper scissors. If you always played one strategy, you would always lose. Therefore, that is not an equilibrium. The only Nash Equilibrium that exists in a game of rock paper scissors is to play rock, paper and scissors with an equal probability of [1/3, 1/3, 1/3] ). To calculate the mixed strategy equilibrium, we must find the probability that the female player chooses to split such that it makes the male player indifferent between choosing split and steal. For a more concise and mathematical explanation, please look at the handout here. In any case, I will provide my calculations below (where p is the probability of the female player choosing split).

Male's payoff of "split" against female player choosing (split, steal) with probability (p, 1-p):

p (50,000) + (1-p)(0) = 50,000p

Male's payoff of "steal" against female player choosing (split, steal) with probability (p, 1-p):

p (100,000) + (1-p)(0) = 100,000p

In order for the male to be indifferent between these mixed strategy expected payoffs, his expected payoff from choosing "split" and "steal" must be equal. Hence:

50,000p = 100,000p

=> p = 0

So basically, we learned that both players will choose "split" with a probability of zero in equilibrium. However, this is simply the pure strategy equilibrium of both players choosing "steal." This makes intuitive sense, because the player would only get lower payoffs by choosing "split" were the other player ever irrational and decided to choose "split." This goes back to the domination argument. However, given the case of multiple Nash Equilibria, we must check to make sure that there are no mixed strategy equilibria.

Now you may be thinking that all of this is stupid, because the male player clearly chose "split," a strategy that we said a rational player should never choose. However, the key to this is that we assume the players to be rational. A full analysis of this situation would probably involve a complex discussion that involves behavioral economics. The fact is that a normal person probably doesn't consider the above analysis when making a decision on a game show (but it should perhaps be noted that the outcome is still Nash). However, it does shed some light on the reasons why what the female player did was not, in fact, greedy and corrupt, but simply rational.

Note that this might be slightly different from what you would expect the outcome to be for this game. We are essentially saying that the situation where both players get nothing is rational over the case where both players get half the pot. However, this is no different from our old friend, the prisoner's dilemma. In both of these cases, the outcome is not Pareto efficient (does not maximize total surplus). The potential for higher payoffs ends up reducing equilibrium payoffs to zero.

I'll leave you with another short clip from an episode of "Golden Balls," this time with a slightly different outcome.

A quick glance at the comments show that most viewers were not too pleased with the female player's choice to steal. However, let's take a look at the payoff matrix of this game:

Note that I decided to change the jackpot to 100,000 euros for mathematical simplicity (it's actually 100,150 euros). This situation is slightly different from your typical prisoner's dilemma game, chiefly due to the presence of weak dominance (a case where a the payoff of a strategy is always equal or greater than the payoffs of another strategy as opposed to strict dominance, where the payoff of a strategy is always greater than that of another).

Because the game is symmetrical, I will proceed to analyze the payoffs of only the male player. Note that the payoffs are the exact same for the female player. Given that the female player chooses to split, the best response of the male player is to steal, as a payoff of 100,000 is greater than a payoff of 50,000. If the female player chooses to steal, the male player is indifferent between choosing split or steal. In this game, the male player's strategy of "steal" weakly dominates his strategy of "split."

However, note that this simple analysis is not complete. Because of the existence of weak dominance, two other Nash Equilibria exist: the outcome where the male splits and the female steals, and the case where the male steals and the female splits. If the reason for this is unclear to you, think about the definition for a Nash Equilibrium. The necessary condition for a Nash Equilibrium states that no player can have a profitable deviation. In the outcome where the female splits and the male steals, neither player can increase their payoff by changing his strategy, taking the other player's strategy as given.

The interesting thing about this is that because both "split" AND "steal" are best responses to a particular strategy, the possibility of a mixed strategy Nash Equilibrium arises. A mixed strategy is a scenario where more than one strategy is played at an equilibrium probability (think about a game of rock paper scissors. If you always played one strategy, you would always lose. Therefore, that is not an equilibrium. The only Nash Equilibrium that exists in a game of rock paper scissors is to play rock, paper and scissors with an equal probability of [1/3, 1/3, 1/3] ). To calculate the mixed strategy equilibrium, we must find the probability that the female player chooses to split such that it makes the male player indifferent between choosing split and steal. For a more concise and mathematical explanation, please look at the handout here. In any case, I will provide my calculations below (where p is the probability of the female player choosing split).

Male's payoff of "split" against female player choosing (split, steal) with probability (p, 1-p):

p (50,000) + (1-p)(0) = 50,000p

Male's payoff of "steal" against female player choosing (split, steal) with probability (p, 1-p):

p (100,000) + (1-p)(0) = 100,000p

In order for the male to be indifferent between these mixed strategy expected payoffs, his expected payoff from choosing "split" and "steal" must be equal. Hence:

50,000p = 100,000p

=> p = 0

So basically, we learned that both players will choose "split" with a probability of zero in equilibrium. However, this is simply the pure strategy equilibrium of both players choosing "steal." This makes intuitive sense, because the player would only get lower payoffs by choosing "split" were the other player ever irrational and decided to choose "split." This goes back to the domination argument. However, given the case of multiple Nash Equilibria, we must check to make sure that there are no mixed strategy equilibria.

Now you may be thinking that all of this is stupid, because the male player clearly chose "split," a strategy that we said a rational player should never choose. However, the key to this is that we assume the players to be rational. A full analysis of this situation would probably involve a complex discussion that involves behavioral economics. The fact is that a normal person probably doesn't consider the above analysis when making a decision on a game show (but it should perhaps be noted that the outcome is still Nash). However, it does shed some light on the reasons why what the female player did was not, in fact, greedy and corrupt, but simply rational.

Note that this might be slightly different from what you would expect the outcome to be for this game. We are essentially saying that the situation where both players get nothing is rational over the case where both players get half the pot. However, this is no different from our old friend, the prisoner's dilemma. In both of these cases, the outcome is not Pareto efficient (does not maximize total surplus). The potential for higher payoffs ends up reducing equilibrium payoffs to zero.

I'll leave you with another short clip from an episode of "Golden Balls," this time with a slightly different outcome.

Quantitative Easing Explained

Saturday, January 1, 2011

This video requires at least a bit of background on the debates inside the fed and the concept of quantitative easing, but it gets the job done well (and is pretty funny). Note that you should not take the conclusions drawn in this video as truth, as most of the issues are currently very hotly debated topics in macroeconomics.

Subscribe to:

Comments (Atom)